Why is the media misleading the public about housing?

The housing market is crashing. There are no “green shoots” or “glimmers of hope”; the market is worn to a stump, it’s kaput. Still, whenever new housing figures are released, they’re crunched and tweaked and spin-dried until they tell a totally different story: a hopeful story about an elusive “light in the tunnel.” But there is no light in the tunnel; it’s a myth. The truth is, there’s no sign of a turnaround or a “bottom” in housing at all. Not yet, at least. The real estate market is freefalling and it looks like it’s got a long way to go. So why is the media still peddling the same “rose-colored” claptrap that put the country in this pickle to begin with? Here’s an example of media spin, which appeared in Bloomberg News on Wednesday:

“US home prices rose 0.7 percent in February from the month before, the Federal Housing Finance Agency said in Washington today, a sign that low interest rates may be moderating declines in real estate values. . . . Housing market data indicates prices are starting to “stabilize,” and households’ available cash should improve through each quarter of 2009 and into 2010.” (Bloomberg)

This report is complete gibberish. The only way to get a fix on what’s really happening with housing is to compare prices year over year (yoy) not month to month. Clearly, the journalist decided to spin the story from this angle because it offered the one flimsy sign of hope in a sector that’s been reduced to rubble. But, don’t be fooled, housing isn’t staging a comeback. Not by a long shot.

This is from Marketwatch:

“The Case-Shiller index of 20 major cities fell 2.8% in January, the fastest decline on record. The Case-Shiller index rose more than the Federal Housing Finance Agency (FHFA) index did during the bubble, and it’s fallen faster since the bubble burst . . . The index was down 19% year-over-year in January.”

So, the only reason that housing prices rebounded (slightly) in February was because, one month earlier, they were “declining at the fastest pace on record.” That’s not a sign of “green shoots” like the Pollyannas say. It’s a sign of a ferocious ongoing contraction. The only thing that’s keeping housing from collapsing completely is the Fed’s purchases of Fannie and Freddie mortgage-backed securities (MBS). Bernanke’s action has pushed interest rates to record lows giving homeowners a chance to refinance rather than default on their loans. Struggling homeowners have been granted a one-time reprieve courtesy of the US taxpayer. That’s great, but the fact that the Fed is subsidizing the industry to the tune of $1.25 trillion is hardly cause for celebration. What Bernanke should have done is prevented the credit bubble from inflating in the first place.

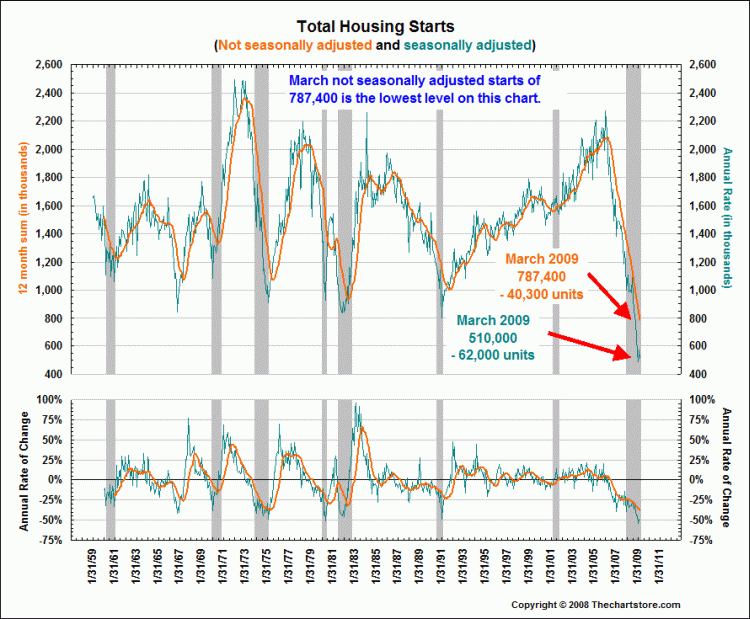

Check out this chart on The Big Picture to see a chilling illustration of a market in

capitulation-phase.

As the caption states:

“We are now in uncharted territory — new home starts have never fallen to these levels for as long as the Commerce Department has been tracking this data (since 1959). Note also the magnitude of the drop — it is unprecedented, having easily surpassed the 1982 collapse, the present circumstances have now become slightly worse than the 1973-75 fall.”

Housing will continue to deteriorate no matter what the Fed does; the downward momentum is too great to resist. And although the refi-business is booming, new home sales are still flat. Buyers are just too scared or too broke to take advantage of the ultra-low interest rates. (4.80%, 30-year fixed) And now that Obama’s foreclosure moratorium is over, delinquencies are stacking up faster than ever before auguring another wave of foreclosures. This is from DataQuick: “Golden State Mortgage Defaults Jump to Record High”:

Lenders filed a record number of mortgage default notices against California homeowners during the first three months of this year, the result of the recession and of lenders playing catch-up after a temporary lull in foreclosure activity . . .

A total of 135,431 default notices were sent out during the January- to-March period. That was up 80.0 percent from 75,230 for the prior quarter and up 19.0 percent from 113,809 in first quarter 2008, according to MDA DataQuick.

And from Bloomberg:

Fannie Mae and Freddie Mac mortgage delinquencies among the most creditworthy homeowners rose 50 percent in a month as borrowers said drops in income or too much debt caused them to fall behind, according to data from federal regulators.

The number of so-called prime borrowers at least 60 days behind on mortgages owned or guaranteed by the companies rose to 743,686 in January, from 497,131 in December, and is almost double the total for October, the Federal Housing Finance Agency said in a report to Congress today.

So, even top-of-the-line prime borrowers are having trouble making their payments. The debt virus has now spread to all loan categories. But what about Obama’s mortgage relief program? Won’t that help keep people in their homes?

In the last two months, roughly 9,000 mortgage modifications have been worked out under Obama’s Streamlined Modification Program. At the same time delinquencies have increased by roughly 195,000 per month. That means there are 186,000 more delinquencies than modifications per month. Obama’s program is like a re-staging of grunting Sisyphus pushing his boulder up the hill — utter futility.

Many economists believe that “cramdowns” are the only way to slow the rate of foreclosures and stop the precipitous decline in housing prices. Cramdowns allow a judge to modify mortgages by marking down the face value (the principle) of the loan. When mortgages accurately reflect current market prices, people tend to stay in their homes. But when prices fall sharply and homeowners owe more on their mortgage than their home is worth, (negative equity) they simply stop making their payments and leave.

So far, cramdown legislation has passed the House, but has stalled in the Senate where it looks like it will be defeated. Powerful groups of bondholders have taken their case to Capital Hill where they’re waging a pitch battle against the Obama plan. At this point, it doesn’t look good for supporters of debt relief even though cramdowns are desperately needed to stop the hemorrhaging of foreclosures.

As we noted in an earlier article, the backlog of homes on the market is still in the vicinity of 10 months. But that excludes the vast “shadow inventory” the banks are keeping off the market. According to SF Gate:

Lenders nationwide are sitting on hundreds of thousands of foreclosed homes that they have not resold or listed for sale, according to numerous data sources. And foreclosures, which banks unload at fire-sale prices, are a major factor driving home values down.

“We believe there are in the neighborhood of 600,000 properties nationwide that banks have repossessed but not put on the market,” said Rick Sharga, vice president of RealtyTrac, which compiles nationwide statistics on foreclosures. “California probably represents 80,000 of those homes. It could be disastrous if the banks suddenly flooded the market with those distressed properties. You’d have further depreciation and carnage. (“Banks aren’t Selling Many Foreclosed Homes,” SF Gate)

Inventory has dropped from its peak in 2008, but if the estimates of the shadow inventory are accurate, then the backlog of vacant homes is still about the same. Any recovery in housing will show up first as falling inventory, since the heart of the problem is oversupply.

On Wednesday, the New York Times reported that fewer people are moving because of the troubles in housing. In fact, “Fewer Americans moved in 2008 than in any year since 1962, according to census data released Wednesday, and immigration from overseas was the lowest in more than a decade. . . . It shows that the U.S. population, often thought of as the most mobile in the developed world, seems to have been stopped dead in its tracks due to a confluence of constraints posed by a tough economic spell.” (Sam Roberts, “As housing Market Dips, more in US are Staying Put,” New York Times)

Diminished mobility is just another of the unpleasant side effects of the housing bust.

The problem with housing goes far beyond the supply/demand imbalance. True, buyers are staying away because they know that prices could fall another 15 to 20 percent, but there’s more to it than just that. The housing crisis has been a shock to the psyche. The dream of home ownership — which is so closely linked to the so-called American dream — has turned into a nightmare. The trauma of watching one’s life savings and retirement vanish in a matter of months is devastating. It’s not an experience that’s easily forgotten. Naturally, people will be more skeptical in the future about seductive interest rates and other faux inducements. Keep in mind, that after investors were burned for $7 trillion in the dot.com swindle, tech stocks swooned and the NASDAQ plunged 80 percent over the next year and a half. Housing is headed down that same bumpy path. There probably won’t be an uptick in housing until the market is flat on its back and given up for dead.

New Home Sales Update: On Friday, stocks skyrocketed on news that “new home sales did not fall as far as expected.” Once again, the story was presented in a way that suggested the housing market is “stabilizing”. But a closer examination of Friday’s data reveals how the media has manipulated the facts to create the impression that things are getting better. But they are not getting better; they’re getting worse. Here is a summary of Friday’s “good news”:

1) The median price of a new home fell $201,400 year over year (YOY)

2) Sales of new homes were down 31 percent from March 2008. They reached a record 1.389 million in July 2005.

3) Distressed properties accounted for about 50 percent of all sales.

4) Inventory (new homes) is still bulging at 10.7 months

5) Foreclosures are at record highs